Summary:Digital-only banks are landing more than four of every 10 new checking account openings. To better compete, CFIs can strengthen their online and mobile account opening tools.

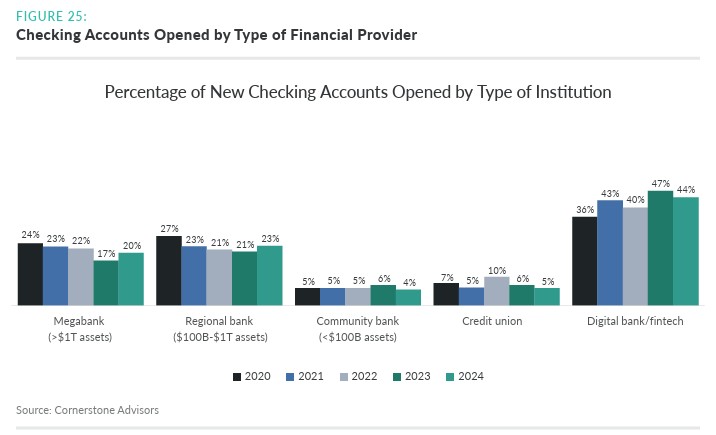

People’s attention spans are getting shorter — we’ve all heard that. But what’s usually missing in that remark is the context of just how much our attention spans have been trimmed down and how quickly the change has happened. In 2004, the American Psychological Association clocked the average attention span on any screen to be around 2.5 minutes. In 2012, the time dwindled down to 75 seconds. As of 2023, our attention span has plummeted to around 47 seconds on average. Ironically, a person can’t expect to get much done in 47 seconds, but that’s what your brand has to work with to engage a potential customer. When a customer is completing a big task like onboarding and opening an online account, it’s a pretty unrealistic metric to try to achieve that in the same 47 seconds. However, the closer you can get, the fewer prospective clients will abandon the process in search of an institution with a smoother process. Online or mobile checking account opening continues to grow, but community financial institutions (CFIs) are being left behind, according to the 2025 Cornerstone Advisors Digital Banking Performance Metrics. Looking at data from the past 5 years, digital banks and fintechs now account for most new checking account openings, followed by large and regional banks. Not much is left for CFIs. Although neobanks and digital banks are a relatively new development, they quickly emerged as leaders in opening new checking accounts. By 2020, they gained more than one-third of all new checking accounts opened, rising to 47% in 2023 before slipping back to 44% in 2024. CFIs, meanwhile, settled in at about 5% of new account openings and haven’t budged much in the last four years. Credit unions ranged from a high of 10% in 2022 to a low of 5% in 2024. Megabanks have slipped somewhat from 24% in 2020 to 20% in 2022, while regionals have bounced around the low 20%, settling at 23% in 2024.081125 Cornerstone advisors chart.jpg39.03 KB

A big part of the problem for CFIs may be the nimbleness of the digital account opening processes at digital-only financial services companies. For example, online banks like Chime and Sofi say that their new account application process takes less than 3 minutes. That’s a tough standard for a CFI to match.Online Account Opening Strategies for CFIs CFIs that want to increase their pool of checking accounts, particularly with digital-savvy younger generations, should probably look to enhance their digital account opening processes. Much of the growth in checking accounts has come from fintechs and online banks, which are adept at the online account opening process.The problem is that many CFI online account opening processes have too much “friction”. The lengthy, detailed application process wears down applicants and prompts them to abandon the task. According to one analysis, half of all applicants call it quits before completing the online application process.Marketing that stresses a financial institution’s online account opening options won’t be successful if the actual process turns potential customers away. Here are some ways CFIs can improve and enhance their digital account opening processes:

Prioritize speed. Work toward an online application process that takes no more than 10 minutes. Since applicants tend to get frustrated and abandon the process after 10 minutes, a CFI with an onboarding process that takes less time than that will be truly competitive.

Investigate where your friction points are in your digital opening process. If you can identify points at which applicants most often give up, you can focus your attention on improving those moments in the process. You can also research general comments about digital account opening on sites like Reddit or by using a social listening tool that crawls social media and review sites for mentions of your brand.

Use instant digital verification. Instant verification is one of the tools that enables digital banks to accept applications so quickly. Using methods like digital ID scans can enable identity verification in seconds.

Avoid detours. The account opening process should be digitally self-contained so that an applicant doesn’t have to keep leaving to find some document, or deal with multiple redirects to external applications to complete the application.

Streamline instructions. Users shouldn’t have to wade through long, involved instructions on how to apply. Review and edit your instructions with an aim of having short and simple wording for every step.

Conduct tests with real people. User testing can quickly reveal problem areas in an online account opening process. From there, you can revisit pain points testers noted and retest once you’ve addressed them.

Have a strong mobile design. Many applicants now use their mobile devices to apply. Make sure your mobile application process is effective, efficient, and user-friendly.

Once an application has been completed and filed, the crucial final step — approval or denial — should be quick and definitive. However, it shouldn’t cast aside risk management protocols. Devious individuals trying to open fraudulent accounts love the speed and simplicity of online account opening. An effective online account opening process should be both fast and safe for the sake of both the applicant and the bank. Speedy online account opening has helped power the rise of digital-only banks. To effectively compete for new accounts, CFIs need equally speedy and straightforward digital account opening processes that work equally well across many digital devices.

Passkeys: Cutting Fraud, Friction, and Support Costs Passkeys provide device-bound, phishing-resistant login that improves security, lowers help‑desk and fraud costs, and gives CFIs a smoother, more modern digital banking experience.

How CFIs Are Modernizing Without Starting Over Replacing a core isn't the only path to modernization. We explore how AI, APIs, and data modernization are helping CFIs build on existing technology and introduce new capabilities incrementally.

This website uses cookies to provide a personalized, informative web experience,

and to support our daily operations with your financial institution.

PCBB does not share or sell your data to other parties.

Please read our Privacy Notice to learn more about the information we collect.