Summary:The 2025 DFAST credit stress testing results show reduced capital strain and regulatory momentum toward smoother stress testing — important signals for CFIs.

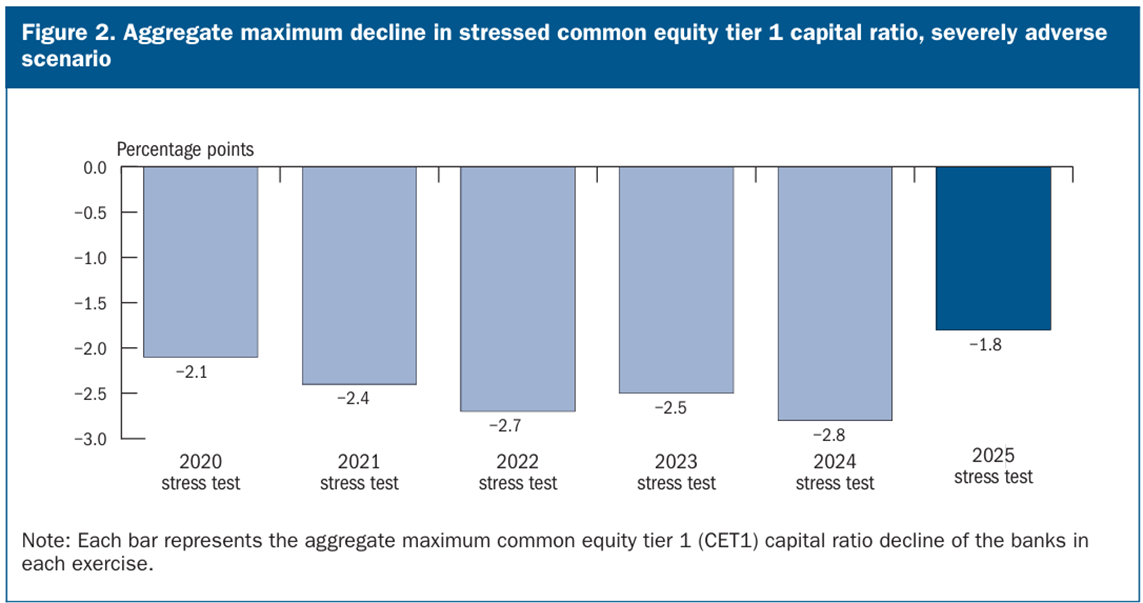

In the 1990s, a Japanese train engineer discovered that the kingfisher bird could dive into water with barely a splash. This observation inspired the redesign of Japan’s bullet trains to reduce tunnel boom and increase speed, simply by mimicking the bird’s beak.The lesson here for community financial institutions (CFIs) — even the most complex systems can benefit from streamlined, low-impact solutions. The Federal Reserve’s latest stress test results suggest a shift toward a less jarring approach in assessing capital strength — one that could make waves in how community financial institutions (CFIs) think about capital planning and resilience.Beneath the surface, this year’s stress test outcomes and the regulatory response offer important cues for how CFIs might approach capital planning going forward — with more flexibility, clearer signals, and smarter modeling that’s tailored to their scale.Lots of Breathing RoomReleased in June, the 2025 DFAST revealed that all 22 participating large banks would remain well capitalized under a severely adverse economic scenario. The average projected decline in common equity tier 1 (CET1) capital was just 1.8%, significantly less than the 2.8% drop forecasted in 2024. Much of this improvement stemmed from stronger pre-provision net revenue (PPNR), a reflection of better earnings in 2024, as well as less aggressive credit loss assumptions, especially in commercial and industrial loans, credit cards, and commercial real estate (CRE).image.png133.37 KBSource: 2025 Federal Reserve Stress Test Results While these outcomes are encouraging, they also highlight the stress test framework’s volatility. Changes in projected losses and income can swing widely from year to year, in part due to the “momentum effect,” where strong past performance leads to more favorable forward-looking assumptions. This makes capital buffers reactive, rather than reliably forward-looking. Recognizing this challenge, the Federal Reserve proposed in April that they would average stress test results over two years in an effort to reduce volatility in capital requirements and offer more planning predictability.Shifting to Banking StabilityIn its July announcement, the Federal Reserve reaffirmed its proposal to average stress test results over two years, aiming to reduce year-to-year volatility and bring greater transparency to the process. Vice Chair for Supervision Michelle Bowman called the move “an important next step” in improving the consistency and reliability of capital planning.While the averaging rule would apply only to large banks under DFAST, its implications reach further. The underlying shift toward clearer and more stable capital expectations matters to institutions of all sizes. For CFIs, it signals that regulators are open to recalibrating how capital buffers are set, potentially paving the way for more tailored, proportional frameworks.Smaller institutions that build credible, scenario-based capital models today may be better positioned tomorrow — whether through engagement in policy discussions or participation in future capital relief or buffer flexibility programs. Being proactive now could pay off later, as the regulatory environment becomes more adaptive to risk and scale.Practical Stress Testing Tips for CFIsWhile formal supervisory stress testing is typically reserved for the largest institutions, the insights from DFAST and regulatory guidance offer a roadmap that smaller community financial institutions can adapt to their own scale. Stress testing doesn’t have to be complex or costly to be effective. In fact, CFIs are uniquely positioned to apply these principles in more targeted, relationship-informed ways. Here are four actionable strategies CFIs can implement to improve capital resilience:

Use large-bank results as stress benchmarks. The 1.8% decline in CET1 capital projected by the 2025 stress test offers a concrete reference point. CFIs can use this figure to reverse-engineer implied stress impairments, applying it to their own capital base to simulate similar downturn scenarios. This approach — grounded in observable peer data — can help estimate the level of capital erosion a CFI might face under comparable economic stress, without the need for complex modeling tools.

Expand scenario planning to emerging risks.The FDIC’s guidance already recommends community banks with significant CRE or subprime exposure conduct portfolio-level testing. However, institutions can go further by modeling risks that reflect today’s evolving landscape, including cyberattacks, AI-driven disruption, rapid interest rate changes, or sector-specific shocks. Simple spreadsheet models that simulate loss rates or revenue pressure can help uncover blind spots and build preparedness.

Tailor testing to your unique portfolio. Stress testing is most effective when it reflects the specific concentrations and vulnerabilities in an institution’s balance sheet. For example, CFIs with heavy exposure to CRE or construction lending could stratify their portfolios by debt-service coverage ratio and loan-to-value bands to identify at-risk segments. Reverse stress testing — or identifying what magnitude of losses would push capital ratios below regulatory minimums — can also help institutions quantify their buffers and inform contingency planning.

Turn stress test insights into better decisions. Stress testing shouldn’t be a standalone exercise. The FDIC notes that community banks with strong integration between stress testing and capital planning tend to outperform their peers, especially during periods of economic disruption. Including stress test outcomes in board reporting, risk tolerance discussions, and loan policy reviews can elevate these exercises from technical compliance to strategic foresight.

More Than a Mere Regulatory ExerciseThe 2025 DFAST results underscore that even the most sophisticated, well-capitalized banks can benefit from sharper scenario design and stable capital expectations. For CFIs, stress testing is not just a checkbox — it can and should be a practical, adaptable tool smaller institutions use to safeguard capital, improve planning, and navigate uncertainty.For CFIs with concentrated portfolios or exposure to localized economic fluctuations, stress testing offers a way to translate risk into insight. When done thoughtfully, it can reveal hidden vulnerabilities, sharpen board-level decision-making, and justify prudent changes in credit, capital, or lending strategies.Crucially, stress testing doesn’t have to be resource-intensive to be effective. From peer-based benchmark modeling to simple spreadsheet scenarios, tools are already available and scalable to your institution’s size and complexity.The key is making stress testing part of the ongoing conversation around risk, growth, and resilience. By embedding stress testing into your strategic toolkit, you can build confidence among directors, regulators, and customers alike — and better prepare for the next period of stress, whenever it comes.

What the Sober Trend Means for Your Loan Portfolio As US alcohol consumption declines, CFIs face rising lending risk in brewery, distillery, and bar portfolios. Lenders should consider stress-test for saturation, margin pressure, and inventory risk, while favoring borrowers with diversified, experience-driven revenue.

This website uses cookies to provide a personalized, informative web experience,

and to support our daily operations with your financial institution.

PCBB does not share or sell your data to other parties.

Please read our Privacy Notice to learn more about the information we collect.