Summary:The FDIC has released its quarterly banking profile for Q2 2025. We review the key data and what it tells us about the health of community banks.

The first reliable health check for blood pressure — the mercury sphygmomanometer — was invented in 1896 by the Italian doctor Scipione Riva-Rocci. His device, with its inflatable arm cuff and mercury column, marked the beginning of routine and non-invasive blood pressure measurement. Just as medical professionals use vital signs to assess patient health, financial analysts and supervisory authorities rely on a set of indicators to gauge the “vital signs” of a bank’s financial health, like those published by the Federal Deposit Insurance Corporation (FDIC) in its quarterly banking profile. For Q2 2025, the FDIC reported data on 4,421 banks, including 3,982 community banks — a decrease of 38 community banks from the previous quarter. This change reflects banks transitioning into or out of community bank status, as well as mergers and acquisitions. Yet, the overall report indicates that community banks remain financially strong and are navigating challenging economic conditions effectively. Here are some key takeaways from the report.1. Profitability has improved significantly.

Net income rose to $7.6B, up $842.9MM (12.5%) over the previous quarter and 22.9% YoY.

Pretax return on assets climbed 15bp from Q1 to 1.33%.

Net interest income increased by $1.2B (5.7%) and noninterest income rose by $483.3MM (10.1%), more than offsetting higher noninterest expense (up $612.7MM, or 3.5%) and provision expense (up $311.5MM, or 29.2%).

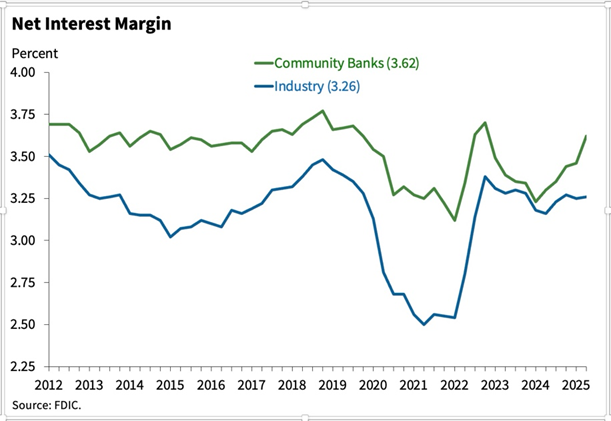

Net interest margin (NIM) rose to 3.62%, up 16bp from the previous quarter. This marked the fifth straight quarterly increase, bringing it close to the pre-pandemic average of 3.63%.

image.png98.96 KB Source: FDIC Q2 2025 Community Bank Charts and Data Community banks’ profitability is showing signs of strength. Higher margins, rising interest and noninterest income, and improving ROA all point to healthier earnings capacity. Importantly, revenue growth is outpacing expense growth, suggesting profitability gains are not just rate-driven but also operational. With NIM approaching pre-pandemic averages, it looks like earnings resilience has largely returned to its historical baseline.2. Asset quality remains sound.

The past-due and nonaccrual loans (PDNA) ratio fell to 1.27%, a reduction of 6bp. Loan balances past due decreased by $886.1MM, driven largely by improvements in 1-4 family residential, farm, and commercial real estate (CRE) loans.

The net charge-off ratio (NCO) ticked up 3bp over the last quarter to 0.19%, slightly above the pre-pandemic average of 0.15%, with CRE-related charge-offs accounting for a large portion of the hike. The NCO ratio is notably lower than the industry at large (0.6%).

Community bank asset quality is sound and improving in most areas, with fewer delinquent loans. However, while significantly lower than the industry, the modest but persistent increase in charge-offs — especially in CRE — suggests there may be some issues bubbling under the surface.3. Loan growth is strong, but deposits — while still growing — are losing momentum.

Total assets increased 0.5% in the last quarter and 4.1% in the last year.

Loans and leases grew $32.3B (1.7%) in Q2 and $90.1B (4.9%) YoY, with the highest YoY increases in nonfarm nonresidential CRE.

Domestic deposits increased $1.8B (0.1%) over the quarter and $114.6B (5.2%) YoY. There were small declines in both uninsured and insured deposit categories.

Community banks are outperforming the industry in loan growth YoY, especially in CRE and residential mortgages. However, deposit growth slowed down in Q2, lagging the industry and raising potential funding challenges. If loan growth continues to outpace deposit inflows, community banks may face pressure on margins and greater exposure to interest rate risk.4. Capital positions are strong.

Tier 1 risk-based capital ratio was 14.1%, up 5bp in the quarter for community banks that don’t participate in the community bank leverage ratio (CBLR) framework. CBLR banks, instead, stood at 12.42%, up 12bp in Q2. Overall leverage was 11.0%, up 10bp from the previous quarter.

Community banks’ capital positions improved in Q2, boosting their resilience against credit, interest rate, and liquidity risks, while also supporting continued lending growth.5. Unrealized losses are trending down.

Unrealized losses on securities declined by $1.7B (3.8%) from the previous quarter, totaling $41.3B. That marks a 20.8% reduction from Q2 2024, just shy of the industry decrease (22.9% YoY). Both held-to-maturity and available-for-sale portfolios saw improvements.

Securities portfolios are in a healthier position than a year ago, with significantly lower unrealized losses. This eases capital and liquidity pressures, giving institutions more balance sheet flexibility. Although the absolute level of unrealized losses ($41.3B) remains elevated by historical standards, most institutions are well capitalized, reducing the risk that these losses will be realized across the board.Community banks are demonstrating resilience in the current economic environment. With rising profitability, sound asset quality, robust loan growth, and strong capital positions, they are well-positioned to support their customers. Although challenges remain, the sector’s overall health suggests that community banks can continue to navigate uncertainty effectively, maintaining their critical role in the US financial system.

H2 2026 Outlook: Mixed Signals for Community Bank Earnings Q1 saw NIM compression and strong loan growth. Now, with rate expectations flipping from cuts to a possible hike by year-end, here’s what CFIs need to think through going into H2.

Succession Planning as a Strategic Advantage for CFIs Bank Director's 2026 Compensation & Talent Survey reveals that just 9% of CFIs have a CEO succession plan and timeline in place. We explore the survey's findings and what CFIs can do to strengthen their succession planning.

This website uses cookies to provide a personalized, informative web experience,

and to support our daily operations with your financial institution.

PCBB does not share or sell your data to other parties.

Please read our Privacy Notice to learn more about the information we collect.