Summary:Onboarding is where loyalty begins. By combining automation, personalization, and transparency, CFIs can turn new customers into long-term advocates who drive growth.

In 1972, the video game Pong hit arcades and introduced millions of people to interactive digital entertainment. The gameplay was simple — two paddles and a bouncing ball — but its genius lay in its ability to draw players in quickly. Within minutes, anyone could understand it and get hooked. That early engagement helped Pong launch the entire video game industry, because first impressions matter. In banking, the first 90 days of a customer relationship can be just as defining. According to J.D. Power, early experiences strongly shape long-term loyalty and advocacy, and Accenture also finds that banks with best-in-class onboarding grow revenues up to 1.7x faster than peers. Yet, many community financial institutions (CFIs) still treat onboarding as paperwork, not as the start of a relationship. To compete effectively and reduce costly attrition, CFIs must rethink customer onboarding as a moment to build trust, demonstrate value, and spark loyalty from day one.Why Customer Onboarding Matters More Than EverThe banking industry is at a crossroads. Digitalization has made banking more transactional, and Accenture’s report shows that 73% of consumers now engage with multiple banks, while one in three maintains a relationship with a digital-only institution. This growing trend isn’t likely to change — and if CFIs don’t connect quickly, they raise the risk of early churn. With the cost of winning new customers climbing, customer replacement becomes far pricier than investing in retention and relationship growth from the beginning.At the same time, customer expectations are rising. Chase reports that 86% of consumers would prefer a single app for all banking needs, while fraud losses could exceed $40B by 2027, if institutions fail to secure the customer journey. In this environment, onboarding is no longer a back-office process — it’s the foundation of long-term engagement.When done right, onboarding should achieve three critical goals:

Reduce friction so customers feel immediate ease.

Build confidence in security and transparency.

Introduce value-added tools that deepen the relationship.

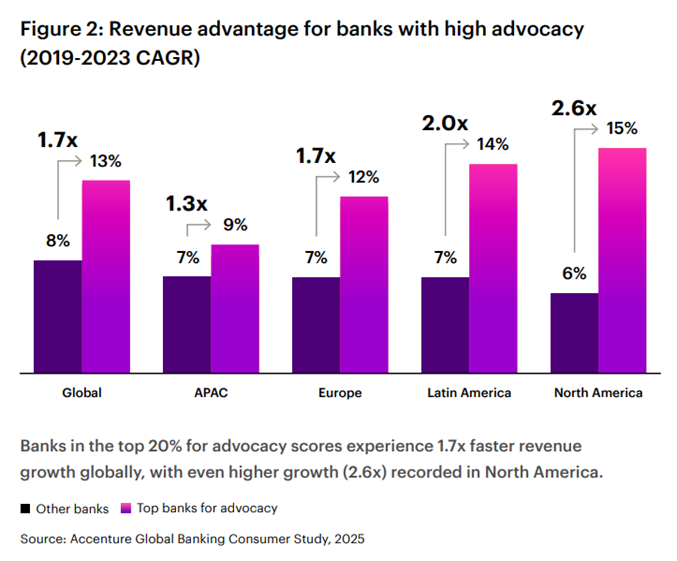

Four Key Strategies of CFI Onboarding SuccessTo transform customer onboarding from a routine process into a loyalty-building experience, CFIs should focus on four interconnected strategies that balance efficiency with personalization.1. Map the First 90 Days Around AdvocacyAccenture’s research highlights that true growth comes not from loyalty alone but from advocacy — customers who not only stay but recommend their institution to others. Advocates hold 17% more products with their primary financial institution and deliver a 5%-30% higher share of wallet.image.png125.45 KB

For CFIs, this means onboarding should go beyond simple account setup and digital solutions. Instead, map the first 90 days with deliberate touchpoints that align with advocacy drivers:

Reassure. Provide transparency on fees and security.

Remember. Personalize interactions based on customer type.

Delight. Offer proactive service and easy digital tools.

Reward. Recognize early engagement, such as savings behaviors.

A structured customer onboarding journey is more than just a one-and-done process — it should ensure brand consistency while signaling to every customer they are valued and understood.2. Automate Carefully with a Human TouchAutomation can certainly streamline onboarding, but it shouldn’t feel impersonal. J.D. Power found that banks improved satisfaction significantly by educating customers on fee structures and resolving issues quickly. Indeed, banking customers who had problems resolved within a day saw a 246-point boost in overall satisfaction.CFIs can use modern automation solutions to:

Send digital welcome kits with clear next steps.

Automate checklists and follow-ups to ensure no step is missed.

Use CRM triggers to prompt staff for personalized outreach when needed.

Alert customers whenever there’s a red flag on their account or spending.

The goal is not to replace human interactions, but to be realistic about digital banking trends, while freeing up staff time for higher-value conversations, ensuring customers feel supported without delay.3. Embed Security and Transparency from Day OneFraud prevention is no longer optional in onboarding — it’s expected. In 2024 alone, the FTC logged 290K cases of identity theft and over 117K incidents of credit card fraud. Unsurprisingly, today’s banking customers want both strong safeguards and clear communication around how their personal data is used.CFIs can differentiate themselves from the competition in several ways:

Implement digital ID verification and address autocomplete for smoother, safer account setup.

Educate customers on fraud prevention tools and best practices during onboarding, especially when it comes to social engineering scams.

Be transparent from the get-go about personal data usage and how sharing customer data can improve personalization.

By addressing fraud concerns head-on, CFIs not only reduce risk but also build trust quickly — an essential foundation for banking loyalty.4. Showcase Tools That Spark EngagementJ.D. Power found that customers who are aware of their financial health tools, like credit monitoring and budgeting apps, had 96 points higher satisfaction than those who remained unaware of their options. Similarly, the Financial Brand notes that banking customers are constantly seeking consolidated digital experiences and richer app functionality.

This is a prime opportunity for CFIs to introduce:

Budgeting and savings tools directly within onboarding flows.

Automated financial check-ins at 30, 60, and 90 days and beyond.

Guidance on how to maximize mobile app features, from goal-setting to direct deposit allocation.

The first 90 days are when customers decide whether to keep or abandon financial tools. Ensuring they experience as much value as possible early on increases adoption and boosts retention.Winning Loyalty Where It BeginsSimply put, the first 90 days aren’t just a test of efficiency — they’re a chance to build lasting advocacy, trust, and profitability.By turning onboarding into a loyalty engine, CFIs can:

Reduce attrition, improving cost efficiency while allocating spend more judiciously.

Increase cross-sell opportunities through personalized introductions and follow-ups.

Generate organic growth through word-of-mouth advocacy and social media engagement, such as via promotional campaigns.

Regional leaders in the J.D. Power study — often smaller community banks — show that personalized service can often outshine scale. This is where CFIs already excel, and leaning into more modern onboarding systems amplifies their existing strengths.By meticulously mapping the customer onboarding journey, automating parts of the process with care, embedding up-to-date security, and showcasing useful digital tools that add value, CFIs can turn new customer relationships into lasting partnerships. Done right, onboarding is not a cost center, but the foundation for growth in a competitive, customer-first era.

Two Conversation Methods to Unlock Cross-Selling Potential Learn the FORD and HEFE methods to improve customer engagement by starting meaningful conversations. These simple yet effective techniques could enhance relationships and potentially increase sales.

M&A Case for a Customer-First Playbook Mergers put customer relationships at risk, but retention is manageable with the right strategy. We look at customer-first strategies and how one CFI developed a playbook to swear by.

This website uses cookies to provide a personalized, informative web experience,

and to support our daily operations with your financial institution.

PCBB does not share or sell your data to other parties.

Please read our Privacy Notice to learn more about the information we collect.