Summary:In its Voice of Community Banks Survey, BNY uncovers opportunities for CFIs to capitalize on untapped potential in the SMB market.

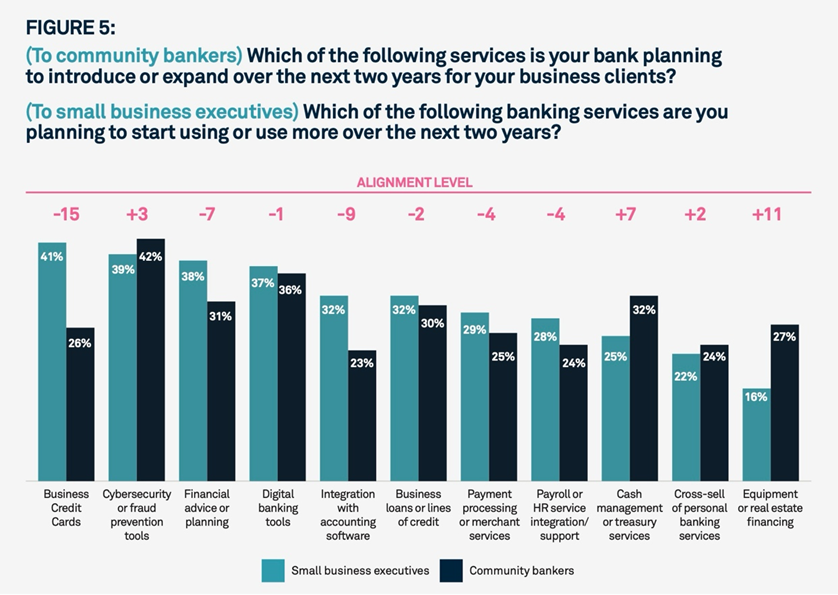

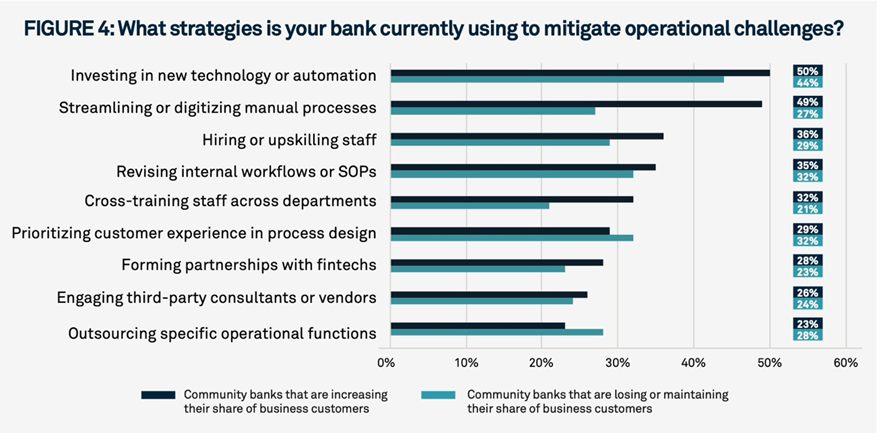

The first modern public opinion survey is generally credited to George Gallup and Elmo Roper in the 1930s, although informal straw polls date back more than a century earlier. Gallup’s American Institute of Public Opinion used scientific sampling to predict election outcomes — and famously got it right in the 1936 US presidential race, forecasting Franklin D. Roosevelt’s win, outperforming the much-hyped but inaccurate Literary Digest poll. In October, BNY released its second annual Voice of Community Banks Survey. This year, BNY interviewed executives from community banks (up to $10B in assets) and small- and medium-sized businesses (SMBs) with revenues between $100K and $50MM to understand the challenges and opportunities they face, what SMBs want from their financial institutions (FIs), and how well community banks are meeting their clients’ expectations. The survey highlights opportunities for community financial institutions (CFIs) in the SMB market and the strategies institutions can use to increase their share of the market.Untapped Potential in the SMB MarketAccording to BNY’s survey, over 70% of SMBs say they either prefer or would prefer to work with a community bank — yet only 31% do so. Half of those have a community bank as their primary bank. Unsurprisingly, the main reason SMBs choose community banks over their larger competitors is personalised service. Based on the data gathered by BNY, the following five strategies could help CFIs capture new SMB customers and deepen their existing relationships.1. Expand your product offerings. The survey revealed varying degrees of alignment between community banks and SMBs regarding current and future service needs. The strongest agreement was around unmet demand for digital payments support, merchant services, and quicker loan approvals. The demand for business credit cards, on the other hand, was significantly underestimated by institutions: only 26% of community bank respondents plan to offer this service, while 41% of SMBs plan to use it. This gap presents a perfect opportunity for CFIs to stand out from their competitors to attract SMB clients. CFIs should consider developing their own business credit card offerings or partnering with others to deliver robust, SMB-friendly credit card programs. Meanwhile, CFIs should ensure they are meeting all their SMB clients’ needs, including merchant processing and integrated payment solutions, positioning themselves as comprehensive, one-stop providers for business transactions, financing, and payment services. image.png300.71 KB Source: BNY 2025 Voice of Community Banks Survey 2. Leverage data and analytics. Recognizing the wealth of untapped data at their fingertips, community bankers taking part in the survey regard data analytics and insights as their greatest opportunity over the next five years. By applying advanced analytics, CFIs can sharpen their understanding of targeted market segments and accelerate geographic expansion, enabling them to pinpoint high-potential SMB niches and customize offerings to meet their unique needs. A data-driven approach allows CFIs to unlock new growth opportunities, capture a greater share of wallet, and deliver deeper, more meaningful value to their customers.3. Focus on operational efficiency. The survey found that over 80% of SMBs had experienced some form of operational inefficiency when dealing with their community bank, such as slow turnaround or poor communication — errors that could be costly. In fact, community banks successfully expanding their SMB customer base are 81% more likely to digitize manual workflows and nearly 50% more likely to invest in new technology or automation to enhance operational efficiency. These results prove that focusing on ways to overcome operational challenges pays off. These findings demonstrate that CFIs should adopt or upgrade digital workflows, automation, and back-office technology to make SMB onboarding, servicing, and transactions smoother and faster, while also cross-training staff, simplifying processes, and fostering a client-centric experience. image.png247.09 KB Source: BNY 2025 Voice of Community Banks Survey 4. Prioritize cybersecurity, compliance, and risk management. More than half (54%) of SMB leaders who left a community bank pointed to security concerns as the main driver. Moreover, community banks gaining SMB customers are far more proactive in strengthening their defenses — conducting significantly more audits and stress testing (63% vs. 38%) and prioritizing employee training (65% vs. 42%) — to enhance security and protect clients. To address SMB concerns, CFIs should promote strong security credentials and fraud-protection capabilities as a clear differentiator, demonstrating transparency around security practices and ongoing investments in cybersecurity. By visibly prioritizing protection and resilience, institutions can strengthen confidence and build deeper trust with their business clients.5. Modernize architecture. Underpinning all these strategies is the need for a fundamental technology shift: moving away from monolithic, legacy banking systems and toward a modern, modular architecture. A modular, API-enabled ecosystem allows CFIs to integrate quickly with fintech partners and third-party providers, accelerating innovation while reducing operational costs. This flexible infrastructure supports everything from real-time payments and automated lending workflows to advanced analytics and personalized digital banking. As SMB clients increasingly value the streamlined services offered by challenger banks, updating legacy systems is a practical step toward enhancing responsiveness and relevance — a competitive necessity.Small businesses continue to value the personalized service that CFIs are rightly known for. To fully capture the opportunity in this vital market segment, CFIs can strengthen their position by expanding their product offerings to better reflect SMBs’ needs, using data and analytics to deliver more tailored experiences, and focusing on operational efficiency. At the same time, prioritizing cybersecurity, risk management, and compliance remains essential. Underpinning all of this is the need to shift toward a modern, flexible, and modular technology architecture that supports seamless integration and future-ready innovation.

Two Conversation Methods to Unlock Cross-Selling Potential Learn the FORD and HEFE methods to improve customer engagement by starting meaningful conversations. These simple yet effective techniques could enhance relationships and potentially increase sales.

M&A Case for a Customer-First Playbook Mergers put customer relationships at risk, but retention is manageable with the right strategy. We look at customer-first strategies and how one CFI developed a playbook to swear by.

This website uses cookies to provide a personalized, informative web experience,

and to support our daily operations with your financial institution.

PCBB does not share or sell your data to other parties.

Please read our Privacy Notice to learn more about the information we collect.