Summary:Regional and national banks have pulled back from multifamily lending, and that’s created an opportunity for CFIs. We discuss how CFIs can thrive in this niche.

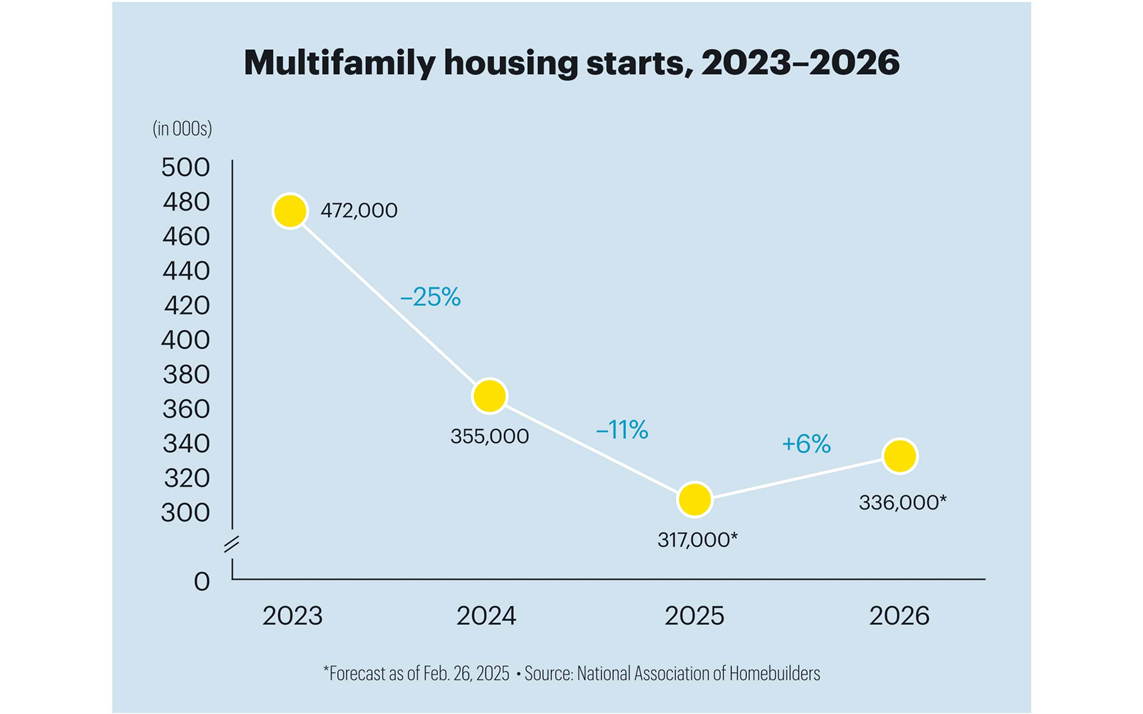

In the world of baking, some of the most celebrated treats owe their success to clever ingredient swaps. When eggs run out, bakers reach for silky applesauce or nutrient-rich flaxseed and water — choices that not only fill the gap, but often add their own unique character and health benefits to the final product. Far from being second-best, these substitutions are embraced by professionals and home bakers alike, and sometimes even become a new favorite method. For example, Greek yogurt as a substitute for buttermilk can produce an exceptionally moist crumb, and coconut oil instead of butter brings a new, delightful flavor.The same logic can be applied to community financial institutions (CFIs) as they step into the void in multifamily lending left by national and regional banks. The larger institutions are lending more cautiously, likely in response to the stress of higher interest rates on existing debt and resulting tighter liquidity. They’re also responding to current conditions in the construction industry itself, which is swimming against a tide of higher material costs, rising insurance premiums, and labor shortages. Recent adjustments to rent stabilization rules in some cities have limited landlords’ ability to increase rental income on their properties. Some geographical areas have too many rentals, so developers must carefully consider the risks that local markets present. While all of these pressures on the multifamily housing market have caused a decline in housing starts, the National Association of Home Builders (NAHB) is anticipating 6% growth in this market in 2026. This potential means CFIs could become part of the comeback of multifamily housing starts.image.png224.68 KB CFIs Fill the Multifamily Lending NeedThese factors have combined to give property owners and developers a dearth of options for financing new construction loans or refinancing existing debt. CFIs have stepped into the gap, expanding relationships and filling a void left by larger banks in CRE and multifamily lending.First and foremost, CFIs are valuable partners to developers and investors because they are willing to lend where larger financial institutions may not be doing business. Yet, they bring other advantages as well. “They’re generally giving us far better terms than we would get from the regionals, and certainly the big national banks,” says Michael Procopio, CEO of Procopio Companies, a development firm in Middleton, Massachusetts. He adds that larger lenders often expect borrowers to fit into their existing programs. CFIs, by contrast, are usually willing to create a structure that can make a loan work, possibly floating, capping, or swapping the rate. “They’re just so flexible, and for us, what that gives us is confidence to close,” Procopio says.Financing for a large apartment building might push up against a CFI’s lending limits, so some local lenders are building participation loans involving multiple CFIs of similar size. A common loan structure might involve an interest-only loan for 48 months, with a 12-month extension option. A borrower that reaches break-even or better debt coverage at that juncture can extend the loan for another 12 months, shifting to a 30Y amortization. According to Independent Banker, most lenders are using loan-to-cost ratios of 60% to 65%.Tips for Succeeding in CRE and Multifamily LendingIn addition to thinking creatively and collaboratively, there are other things CFIs should keep in mind as part of their recipe for successfully lending to CRE and multifamily projects.

CFIs are renowned for their local knowledge. Use what you know of your community to track real estate trends, economic shifts, zoning changes, and areas of demand and oversupply to benefit your business customers and help prevent your CFI from backing a suboptimal project.

Apartment buildings are a classic multifamily build. Don’t forget workforce housing, duplexes and triplexes, affordable housing, senior housing, older properties in need of refreshment, and build-to-rent projects on your list of potential borrowers.

Tax incentives to build affordable housing or redevelop vacant or abandoned property can help fund a project that has a workable ratio of debt to equity.

The Fed will eventually lower interest rates — possibly as soon as this week’s FOMC meeting — and many experts expect the 10Y Treasury to reach 4.08% around Q1’26. Big banks will become interested in CRE and multifamily lending again. By building strong relationships now, CFIs can position themselves to keep many of the business connections they develop.

Big banks have taken a step back from CRE and multifamily lending, probably in response to higher interest rates on existing debt and resulting tighter liquidity, as well as conditions within the construction industry. CFIs have an opportunity to use their local knowledge and ability to build relationships to step into the gap.

How Philanthropy Meets Balance Sheets for CFIs CFIs can create a valuable niche serving nonprofits by providing deposit, lending and advisory services while potentially receiving CRA credit for helping underserved communities.

Turning The Small Business Succession Wave Into Deal Flow A massive SMB succession wave, amplified by the SBA doubling acquisition loan limits, creates opportunity for CFIs. This article discusses how they can make the most of the moment.

This website uses cookies to provide a personalized, informative web experience,

and to support our daily operations with your financial institution.

PCBB does not share or sell your data to other parties.

Please read our Privacy Notice to learn more about the information we collect.