Summary:Rising office vacancies are fueling office-to-residential conversions nationwide. CFIs can finance projects, leverage incentives, and revitalize communities outside urban cores.

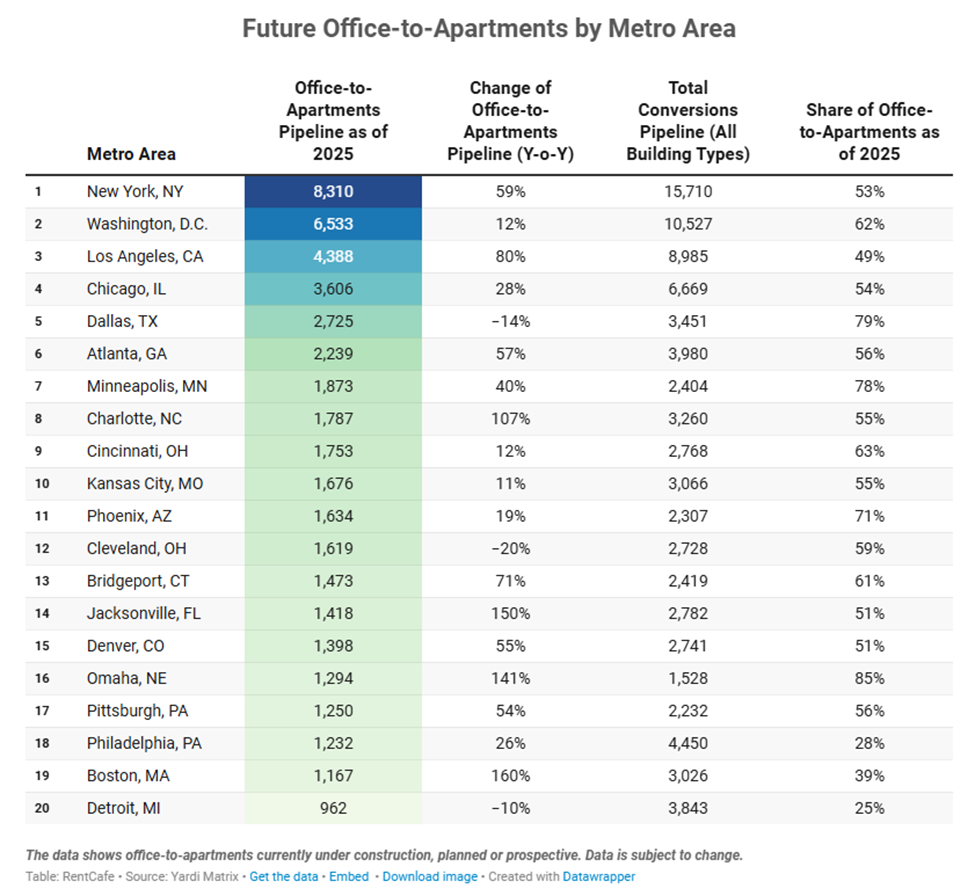

Anyone who wears prescription glasses likely knows the inconvenience of juggling their regular glasses and sunglasses. In the 1960s, two employees at Corning Glass Works, Inc. came up with a solution to this problem by inventing photochromic lenses, which darkened when exposed to sunlight. These are more commonly known today as “Transitions” lenses, after the brand that popularized them. Today, a different type of transition is brewing for community financial institutions (CFIs): rising vacancy rates in offices, which could soon spread beyond urban centers to suburban and rural markets. However, changing commercial real estate (CRE) trends can offer CFIs new opportunities to support the transition of underutilized spaces — but only if they act quickly.The Growing Trend of Office-to-Residential ConversionsAs hybrid work continues to reshape the office market, office vacancies in major cities like New York, San Francisco, and Chicago are reaching unprecedented levels. According to the CBRE U.S. Real Estate Market Outlook, office vacancy rates are expected to peak at 19% in 2025.In response, cities are looking for innovative ways to repurpose underperforming spaces, with office-to-residential conversions emerging as a key strategy. The US now has over 70K office units in various stages of conversion, driven by a growing housing shortage and an oversupply of vacant office buildings. image.png275.63 KBSource: RentCafe While these conversions began in high-density urban centers, they are now expanding into suburban and even rural areas, offering CFIs a chance to support local developers and communities by financing projects that address both the housing crisis and vacant CRE.Emerging Opportunities for CFIsWith office-to-residential conversion activity accelerating and incentives expanding, CFIs that move quickly can secure a competitive advantage while revitalizing underused properties.1. Opportunities in Suburban and Rural Markets

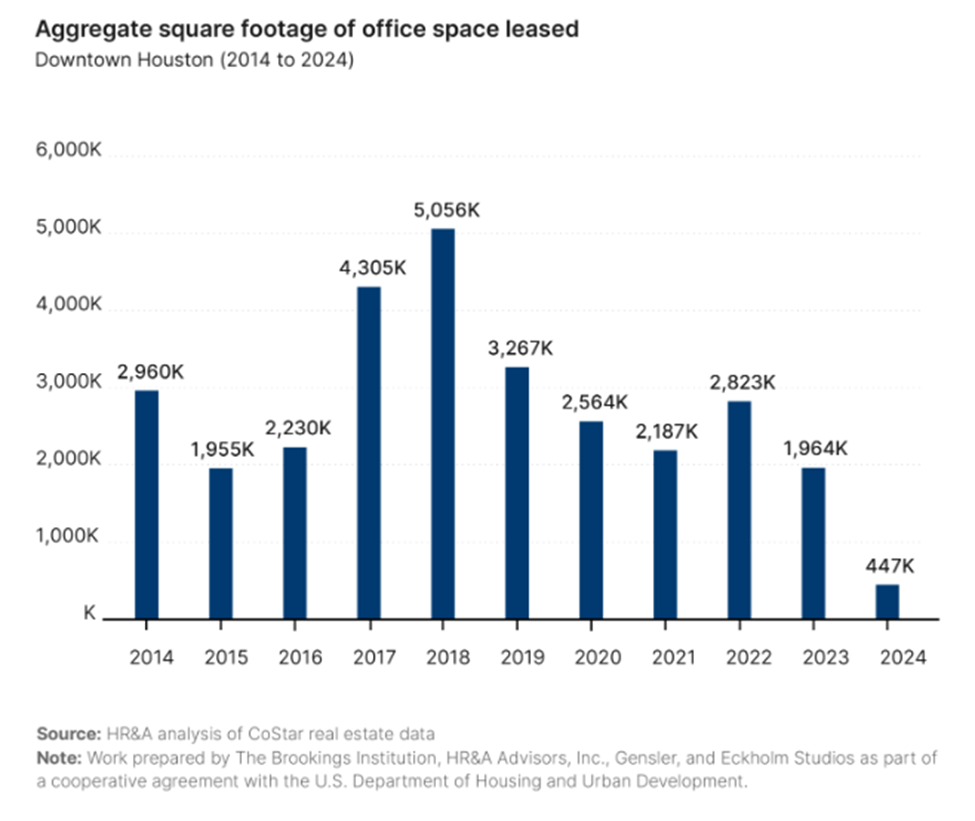

Initially, suburban markets saw rising office demand as companies began decentralizing operations. Yet, with the continued rise of hybrid work, demand for suburban office space is cooling. As office vacancies continue to climb, CFIs should be prepared for a ripple effect. Markets like Omaha and Charlotte have already seen real growth in their office-to-residential pipelines, with projects expanding beyond urban cores. The growing pipelines in these markets is an opportunity for CFIs to support developers with financing options tailored to residential conversions, especially in areas where housing demand is high but supply remains low.2. Leverage Government IncentivesMany cities and states are offering attractive incentives for office-to-residential developers. Boston and Washington, D.C., for example, have launched programs offering funding and tax breaks. By partnering with developers tapping into these government programs, CFIs can access low-risk, profitable lending opportunities, meeting housing demands while minimizing risk, especially in a market where CRE values are in flux.CFIs should also pay attention to tax increment financing (TIF) districts, which have successfully supported residential developments in distressed areas. For example, Houston’s efforts to revitalize its downtown through TIFs illustrate how instrumental CFIs can be in facilitating these types of conversions.image.png154.45 KB Source: The Brookings Institution3. The Growing Demand for Mixed-Use DevelopmentsMixed-use developments that combine residential, retail, and office spaces are very popular these days. More people want to live, work, and play in walkable, vibrant communities, so mixed-use projects are now seen as a sustainable solution to urban sprawl. In fact, according to RentCafe, cities like New York, Los Angeles, and Washington, D.C. are seeing large-scale conversions that include both residential and retail spaces. CFIs should explore opportunities to finance modern, mixed-use projects — especially in suburban and secondary markets — with flexible terms that can help revitalize neighborhoods while meeting the rising demand for affordable housing.4. Assessing Market Conditions and Future RisksWhile the potential rewards of office-to-residential conversions are certainly high, CFIs must also weigh the many risks from all directions. As office vacancies rise, for example, the CECL (Current Expected Credit Loss) model will need to be adjusted to account for potential overexposure risks.CFIs should be proactive in assessing tenant durability and monitoring lease expirations to avoid future revenue cliffs as properties transition from commercial to residential uses. They should also evaluate the stability of suburban office markets. Initially insulated from urban office vacancies, the suburbs are now beginning to feel the same pressures.Key Strategies To Capitalize on Conversion TrendsTo turn market disruption into opportunity, CFIs will need a proactive, targeted approach that balances risk management with creative financing solutions. Here are some suggestions:

Monitor lease expirations and tenant durability. As leases near expiration, CFIs should assess the strength of tenants and determine whether their office space needs will continue to shrink. Early identification will lead to more informed lending decisions.

Stay ahead of CRE market shifts. As hybrid work reshapes the demand for office space, CFIs have to reevaluate their CRE loan portfolios. Stress testing loan assumptions and adjusting underwriting models will ensure resilience despite shifts.

Explore developer financing opportunities. CFIs can play a pivotal role in facilitating office-to-residential conversions by offering tailored financing that aligns with government incentives and developer needs. Flexible loans for mixed-use and residential projects will allow CFIs to meet local housing demands while supporting urban revitalization.

Adapt to emerging sustainability trends. Many office-to-residential conversions will require significant renovations to meet sustainability standards. CFIs can offer green financing products to support developers who are committed to energy-efficient upgrades and environmentally responsible building practices.

Finding Footing in a Shifting CRE LandscapeAs office vacancies rise, CFIs must act swiftly to capitalize on the growing trend of office-to-residential conversions. They offer a unique opportunity to meet the housing needs of growing suburban and rural markets while supporting the economic revitalization of local communities.The shift in office space utilization is reshaping real estate markets nationwide. By staying ahead of market shifts, monitoring lease expirations, and leveraging incentives, CFIs can help shape the future of housing and commercial real estate, like they’ve always done, at the heart of their communities.

Less Risk, More Housing: What Pre-Approved Plans Mean for CFIs Pre-approved building plans can help reduce permitting delays, costs, and construction risk. These plans can help ease America's 4.7M-home deficit while giving CFIs safer lending opportunities and stronger ties to local developers and underserved neighborhoods.

This website uses cookies to provide a personalized, informative web experience,

and to support our daily operations with your financial institution.

PCBB does not share or sell your data to other parties.

Please read our Privacy Notice to learn more about the information we collect.