Summary:Offering insurance services could provide CFIs with opportunities to diversify revenues and strengthen relationships. We look at the challenges and approaches and list some examples of CFIs already in this space.

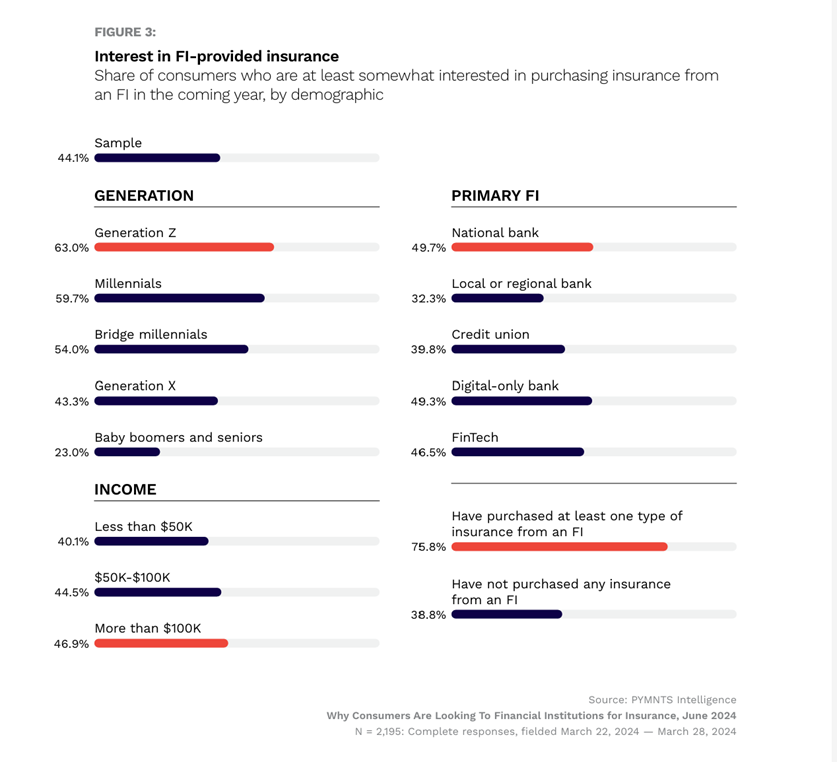

The devastating Great Fire of 1666 in central London in the UK caused estimated damages worth nearly $2B in today’s money. In the aftermath, a wave of reconstruction began, leading to an unexpected development: the birth of modern property insurance. In 1680, the “Fire Office” — one of the modern world’s first insurance companies — was born, and ten years later, one in ten houses in London was insured.A 2024 PYMNTS survey found that 44% of consumers would be interested in buying insurance from a financial institution (FI). This is especially true for younger respondents, who are mostly motivated by convenience. The figure rises to 60% for millennials and 63% for Gen Z. Across age groups, trust in FIs is the most cited reason for preferring FIs for insurance services. That said, over half of consumers don’t know whether their FI offers insurance products.image.png99.42 KB Source: PYMNTS Is insurance an opportunity for CFIs?Since only 15% of consumers currently buy insurance from FIs, according to the PYMNTs study, there is unmet demand and a potential opportunity for community financial institutions (CFIs). As well as meeting their customers’ needs, CFIs might choose to enter this space to diversify their revenue stream and increase noninterest income, helping offset pressure from shrinking net interest margins. Boston Consulting Group believes that retail banks that leverage their data to tailor their offerings and get their insurance model right can boost their profits by 15%-20%. Moreover, offering insurance can help CFIs build deeper, stronger relationships, increasing loyalty and customer lifetime value — more so if they truly leverage their data to present customers with relevant contextual offers, rather than simply making insurance products available on their website. “There are all sorts of transactions or even just opening a savings and checking account for the first time at the financial institution. All of those are excellent opportunities to bring forward, timely and relevant offers to that consumer,” says Mike Mahoney, regional vice president at Franklin Madison, a company that provides insurance products to FIs.What are the challenges, and how can they be overcome?

Despite the benefits, there are some hurdles to be overcome for CFIs considering the insurance space, particularly as they will likely lack in-house expertise:

Regulatory complexity. To provide insurance solutions, FIs need to navigate a dual regulatory framework, at both the federal and state levels, as each imposes its own licensing and operational compliance requirements.

Operational complexity. Selling insurance requires additional staff, training, marketing capabilities, and technology integration. These are often perceived as a barrier to entry.

However, CFIs do not need to build their insurance market presence from scratch. Most CFIs will choose one of two models, or a combination of both:

Partner with a third-party insurance provider. Many CFIs choose this approach for its speed to market, low capital outlay, and access to a full suite of insurance products. Among countless others, Ocean State Credit Union, a $339MM-asset CFI, launched an embedded insurance platform to provide its retail and commercial customers with a wide range of insurance services. “We are excited to adopt Insuritas’ excellent embedded insurance platform to strengthen the portfolio of financial products available to our members as we position ourselves to be their primary financial services provider…and help our members save more on their insurance needs across the board,” said Ocean State Credit Union CEO Michael Garvey.

Acquire an existing insurance agency. In this model, CFIs acquire a separate insurance agency, which can be integrated into the existing business or run as a wholly owned subsidiary. Although capital investment is required, a revenue stream is guaranteed from the get-go. Towne Bank, with $17B in assets, entered the insurance market in 2001, two years after opening. Through a series of acquisitions, it has expanded its insurance services, which it now sees as core to its business. Towne’s insurance revenue reached $118MM in 2024, up 8% from the previous year.

Adopt a hybrid approach. Some CFIs choose to acquire insurance capability to get a head start and then partner with third-party providers to boost their offering. Dollar Bank, a $11.9B-asset CFI, operates a bank-owned agency licensed across multiple states, Dollar Bank Insurance Agency. In recent years, it has expanded its digital offering through a vendor partnership, enabling the CFI to provide a full suite of products supported by live agents. What’s more, this year it partnered with Franklin Madison to deliver a marketing campaign to promote and support a range of client protection solutions. The pilot exceeded projected outcomes by 123% and was instrumental in driving stronger engagement with no capital outlay.

While entering the insurance market offers real opportunities for CFIs to diversify revenue and better serve customers, doing so requires careful navigation of both regulatory and operational complexities. By partnering with third-party insurance providers or acquiring an existing agency, CFIs can leverage external expertise and established infrastructure, making it easier to comply with federal and state regulations, address operational demands, and manage risk. With the right approach and partners, CFIs can integrate insurance offerings into their business models in a compliant and effective manner, enhancing their value to customers while maintaining regulatory integrity.

Turning The Small Business Succession Wave Into Deal Flow A massive SMB succession wave, amplified by the SBA doubling acquisition loan limits, creates opportunity for CFIs. This article discusses how they can make the most of the moment.

Embedding Banking Where Business Happens Commercial embedded banking within enterprise resource planning software or B2B marketplaces represents an explosive lucrative opportunity for the FIs that take advantage of it.

This website uses cookies to provide a personalized, informative web experience,

and to support our daily operations with your financial institution.

PCBB does not share or sell your data to other parties.

Please read our Privacy Notice to learn more about the information we collect.