Summary:De novo applications and new bank launches have been trending up in 2020 and 2021. Favorable signs include rising investor confidence in new banks and government encouragement of new banks in rural and underserved areas. This year, there were nine new banks for every 100 lost, compared to only two banks for every 100 lost during the previous decade. While this is good news, is it a trend? Here is our insight.

If you start a new habit, like exercising every day, it takes time before the habit becomes a long-term behavior. How much time? According to research published in the European Journal of Social Psychology, it could take up to 254 days! But, don’t get discouraged, good habit formation took only 18 days, for some people.While you ponder which category you may fit into, we turn to another type of formation – bank formation. New bank formation is inching upward and could reach higher as several favorable trends continue to point toward more de novo banks in the future. Investors seem to be more interested in participating in new bank formations, while the government has been looking favorably on de novo formation, particularly those focusing on rural or underserved areas. De novo by the numbers

De novo applications all but disappeared after the 2008 recession. They began to edge up again in 2019 but then the pandemic hit. A number of applications were withdrawn and not many new ones were issued. But as the economy began recovering, bank applications resumed. There were 15 banks and savings and loans formed in 2020, after just nine in 2019. Sixteen de novo applications were filed in 2021 through November. Meanwhile, the FDIC had 19 applications under review through November dating back as far as March 2020.Trend or blip?

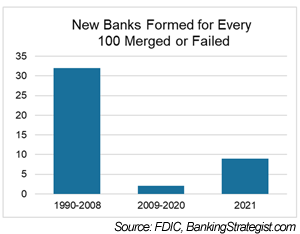

Calling the recent group of new bank applications and formations a significant trend may be a little premature. Mergers are still reducing the number of existing banks and there are far too few new bank formations to replace the loss. Since 1990, more than 2,900 de novo banks opened, but almost all of that activity took place prior to the Great Recession. From 2000 to 2009, an average of 132 de novo banks formed each year. Since then, the average has been just seven per year. Furthermore, merger activity has been brisk for decades, taking out far more banks than are being created. From 1990 to 2008, 32 new banks were formed for every 100 that either merged or failed. From 2009 to 2020, an average of just two new banks formed for every 100 lost. For 2021, the rate has improved to about nine new banks for every 100 lost, but that is still a long way from the 32 average of the earlier period . New-Banks-Formed-Graphic-PCBB-BID-122421-FINAL.png14.93 KBWhy de novo activity is on the rise

Solid investment. Large banks have seen improving financial performance and a rise in stock prices. Smaller banks have seen similar benefits in income and valuations. Those underlying trends are encouraging signs for de novo banks as investors look for solid, stable ways to put their money to work over the long term.

Greater legislative and regulatory support. Another positive is the activity in Congress to encourage new banks in rural and underserved communities by reducing and easing capital requirements. The Promoting Access to Capital in Underbanked Communities Act of 2021 was introduced by US Representative Andy Barr of KY this past spring. Legislation is pending for now on that front. But, there has already been some easing of the regulatory burden on de novo formation in the interest of helping underserved communities.

De novo profits. It also seems that de novos are becoming profitable more quickly. From 2000 to 2009, it took an average of 8.6 quarters for newly launched banks to turn a profit. For the 30 de novos launched between 2010 and 2020, it took 6.8 quarters to reach profitability.

The bottom line is that investors like what they see in the de novo space right now and are backing these startups. It’s far from a stampede, but it is still a positive shift in increasing the number of community financial institutions.

2025 in Review: Part 1 of 2 — An Evolving Market In a two-part series, we look at trends, challenges, and opportunities CFIs have encountered over the past year, and how they have responded to support their continued growth and resilience.

Sell, Buy, or Stay Independent? M&A Considerations According to the Bank Director’s 2026 Bank M&A Survey, the CFI M&A landscape is shifting. Deal activity is still subdued, but interest in community bank acquisitions is rising.

This website uses cookies to provide a personalized, informative web experience,

and to support our daily operations with your financial institution.

PCBB does not share or sell your data to other parties.

Please read our Privacy Notice to learn more about the information we collect.