The classic computer game Tetris — the second best-selling video game series with over 520MM sales worldwide as of 2024 — is the ultimate puzzle of speed and strategy. Differently shaped blocks fall from the top of the screen, and players must twist and fit them into place before the stack gets too high. Small- and medium-sized businesses (SMBs) often face a similar challenge, juggling cash flow, growth ambitions, and unexpected costs. Just like in Tetris, having the right pieces in the right place at the right time makes all the difference — and community financial institutions (CFIs) that offer flexible, timely, and tailored financing can help SMBs thrive.According to the Federal Reserve Banks’ 2025 Small Business Credit Survey that garnered over 6,500 responses, SMBs reported steady YoY growth in both revenue and employment. Despite this stability, many firms continue to face both operational and financial pressures. At the same time, CFIs have been losing market share of SMB lending to large institutions and online lenders. The survey data reveals where the SMB lending gaps lie and the reasons behind them, leaving a goldmine of data for CFIs with keen attention and enough flexibility to pivot their strategy.Here are a few valuable insights from the survey that CFIs can leverage to better support SMBs in addressing their financial challenges:

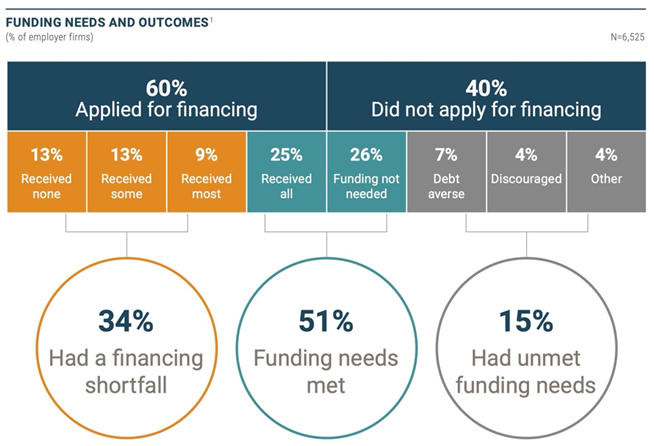

1. Nearly half (49%) of SMBs have either unmet financial needs or a financing shortfall.

- Of the applicants who were not approved for some or all the financing they sought, 46% said lender requirements were too strict.

- Among financing products, business lines of credit were the most commonly sought (43%), followed by business loans (32%) and SBA loans (20%).

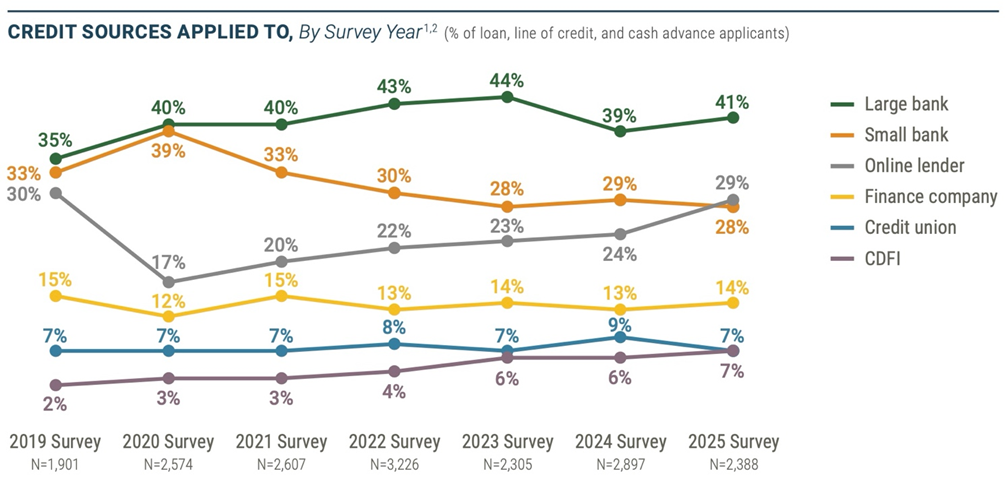

Source: Small Business Credit Survey, Federal Reserve Banks 2. CFIs’ share of the SMB credit market has been decreasing over the years, with large banks and online lenders picking up the business.

- Applicants who turned to online lenders were more likely to prioritize the speed of the application process and the likelihood of being approved.

- Applicants who applied to large or small banks most often chose their lender because of an existing relationship.

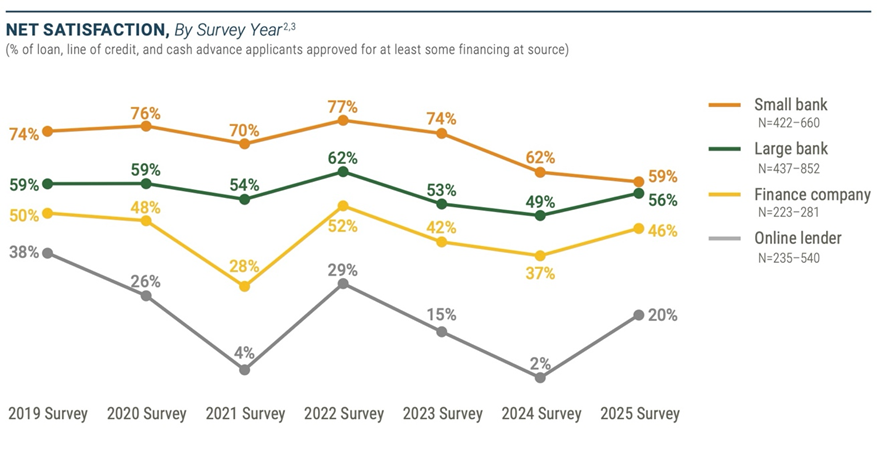

3. Borrowers’ expectations and perceptions often differ from reality.

- Contrary to expectations, applicants at small banks were the most likely to be fully approved (57%), compared with applicants at finance companies (50%), large banks (43%), and online lenders (38%).

- Sixty percent of borrowers who turned to online lenders said their actual borrowing costs exceeded expectations, compared with 37% of those who borrowed from small banks and 31% from credit unions.

- Applicants who sought financing from online lenders were more likely than other borrowers to report problems with their lender, such as high interest rates and unfavorable repayment terms.

- While SMBs’ net satisfaction with CFIs over the years has been declining, at 59% it remains higher than for any other lender, particularly relative to online lenders (20%).

Strategies for CFIs To Boost SMB BorrowingBuilding on these insights, CFIs can adopt several targeted strategies to better serve SMBs and boost borrowing outcomes.

- Increase digitization to speed up the approval process. Faster decision-making is increasingly important for SMB borrowers. By investing in digital applications, automated workflows, and streamlined credit processes, CFIs can shorten approval timelines while maintaining prudent risk controls. Improving speed without sacrificing service quality helps institutions stay competitive with online lenders.

- Explore alternative underwriting models. Traditional credit criteria can limit access to financing for otherwise viable businesses. Expanding underwriting approaches to include cash flow analysis, alternative data, or more flexible risk assessments can allow CFIs to serve a broader range of borrowers while still managing portfolio risk effectively.

- Leverage relationship-based lending. Existing customer relationships remain one of the strongest advantages CFIs have. Proactive outreach, deeper account engagement, and coordinated relationship management can position the institution as the first place a business turns to when financing needs arise. Strengthening these connections can improve both approval rates and borrower retention.

- Offer tailored solutions. Flexible financing options such as microloans, revolving lines of credit, and customizable repayment structures align closely with SMBs’ variable cash flows. By broadening their product set and enabling real time access — such as by offering instant digital drawdowns — CFIs can better meet client needs, capture more underserved demand, and build “stickier” customer relationships.

- Communicate more effectively. Borrowers don’t always recognize the advantages CFIs offer, often assuming other options are faster or more advantageous. By proactively highlighting their strengths — such as personalized service, flexible solutions, transparent terms, and timely approvals — CFIs can address these misconceptions, build trust, and encourage more SMBs to turn to them for their financing.

The Small Business Credit Survey highlights both unmet SMB funding needs and a declining share of the SMB credit market for CFIs, with large banks and online lenders filling the gap. Yet borrowers’ experiences with online lenders are mixed, offering valuable lessons for CFIs. By digitizing processes to speed approvals, exploring alternative underwriting models, leveraging relationship-based lending, offering flexible solutions, and clearly communicating their value, CFIs can strengthen their performance in this segment and better support their SMB customers while also regaining ground lost to other lenders.