Summary:Many businesses still rely on checks for B2B payments. We discuss how CFIs can support check usage among their SMB customers while promoting the adoption of modern payment methods.

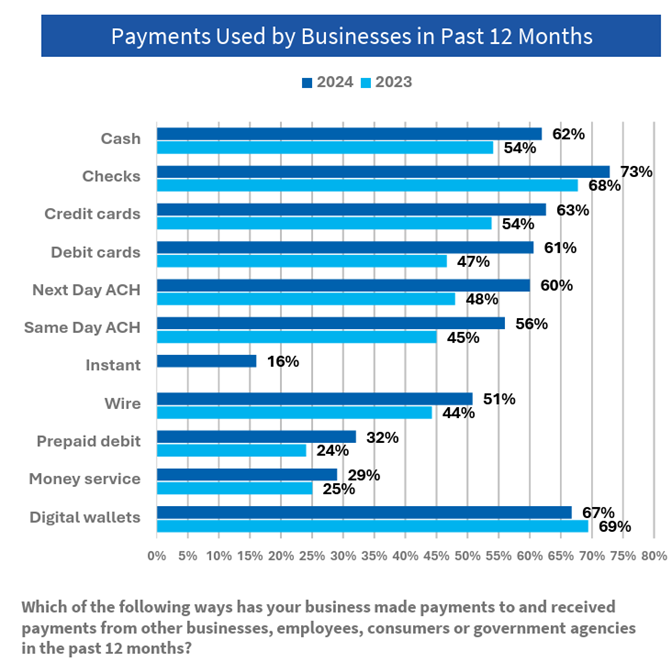

Candles lit the world for thousands of years — until gas lamps began to replace them in the mid-1800s, followed by electric light bulbs in the early 1900s. Yet, instead of disappearing, candles reinvented themselves to become a lifestyle product. Seven in ten American households use candles, and an estimated 1B pounds of wax are used for candle making in the US every year. Similarly, while not reinventing themselves, checks have shown remarkable staying power as the payments landscape has evolved with the rise of digital payments. Despite the obvious benefits of digital payments — including improved cash flow, increased speed, efficiency gains, reliability, and security — US small- and medium-sized businesses (SMBs) still rely heavily on checks. While the use of checks in B2B payments is down, 73% of businesses continue to use this payment method. What’s more, although the number of check transactions has declined over the years, the average value of commercial checks has increased steadily.image.png140.85 KBSource: Federal ReserveAccording to a PYMNTS Intelligence report, the use of digital payments is concentrated in digitally mature sectors, such as gaming and the gig economy. SMBs in these sectors are 45% more likely to use instant payments as their primary ad hoc payment method than firms in less digitally advanced sectors. Moreover, according to the same report, usage appears to correlate with automation — adoption rates are higher among businesses with more automated accounts receivable (AR) systems. Since over four in ten microbusinesses still use manual AR processing, this limits their ability to benefit fully from instant payment capabilities. Why Checks Are So StickyBusinesses that still use checks point to the following reasons for continuing with this payment method:

Control. Writing a check gives the payer some control over when funds leave their account, which is particularly relevant for SMBs with tight budgets.

Legacy processes. Many SMBs have longstanding workflows (accounting, invoicing, supplier relationships, etc.) built around checks, making the transition to digital payments harder.

Paper trail. SMBs often receive detailed remittance information with check payments, which can be difficult to replicate with digital payments.

Supplier preferences. Some suppliers — particularly smaller or more traditional ones — prefer receiving payments by check, so accommodating their preferences is key to maintaining good relationships.

Fees. Despite the efficiencies widely associated with digital payments, 32% of SMBs cite fees as a barrier to adopting instant payments, according to PYMNTS.

Strategies to Fine-Tune the Balance Between Checks and Digital PaymentsCommunity financial institutions (CFIs) should consider nudging their SMB customers towards greater use of digital payments while improving their check processing for those customers who still want to use checks. Here is how they could do this:

Educate SMBs on the advantages of digital payments. CFIs could offer training, webinars, and short videos to demonstrate the advantages of digital payment adoption, focusing on cash flow benefits, cost efficiencies, and fraud detection. For example, research shows that ACH payments are, on average, 5x to 10x cheaper than paper checks. Also, checks remain the payment method most frequently targeted by fraud, with 63% of financial professionals encountering attempted or actual check fraud in 2024.

Ensure digital payments meet SMB needs. As a first step, CFIs should make digital payments simple to adopt — for example, by offering a guided setup process, by assisting with vendor setup, and by providing templates for vendor communication. Since receiving remittance information is a key reason for SMBs to continue using checks, CFIs can steer their customers towards payment options that enable the exchange of remittance information — for example, through services built on the FedNow® Service or RTP® network.

Modernize internal check processing. CFIs can significantly improve check processing by modernizing legacy systems, adopting cloud-based and AI-driven solutions, and consolidating all deposit channels into a unified platform. Automation reduces errors and costs, advanced fraud detection strengthens security, and centralized data provides actionable insights. By upgrading their technology, institutions can process checks faster and more securely, while also providing a more seamless customer experience.

As digital payments continue to improve and businesses increasingly embrace digital transformation, CFIs should encourage their SMB customers to adopt them. Helping them understand the benefits of digital payments, ensuring they are easy to adopt and meet the SMB’s needs, will help nudge them forward. At the same time, CFIs recognize that there is an enduring demand for checks. Modernizing internal check processing will boost security, cut costs, and enhance the customer experience.

Tapping Cross-Border Payment Demand as a Revenue Source Cross-border payment activities are projected to reach $320T by 2032 and SMBs are a rising portion of that activity. Focusing on cross-border payments is a good way for CFIs to expand their revenue sources and to bolster ties to SMB customers.

Helping SMBs Navigate the Payment Last Mile Many small businesses still rely on paper checks, causing cash flow issues and increasing fraud risk. CFIs can help their SMBs get paid faster by offering modern payment solutions.

This website uses cookies to provide a personalized, informative web experience,

and to support our daily operations with your financial institution.

PCBB does not share or sell your data to other parties.

Please read our Privacy Notice to learn more about the information we collect.