Summary:Positive pay can help you flag fraudulent checks before funds are issued, yet adoption rates are just 29%. We discuss the benefits of positive pay and how to increase its usage.

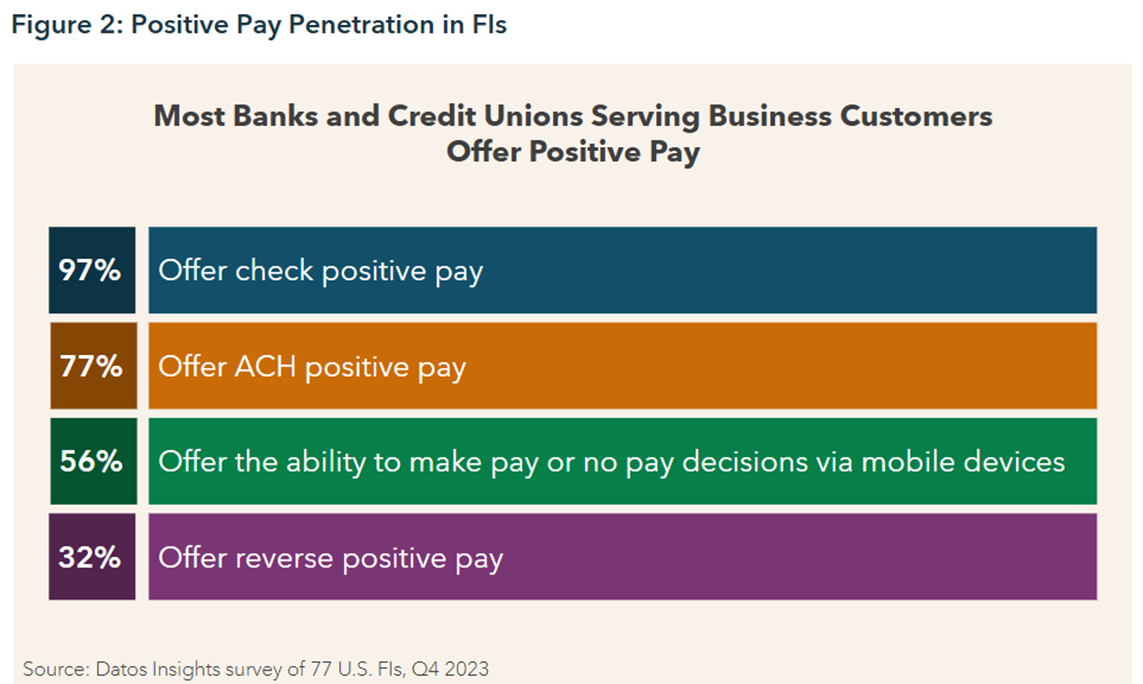

Renowned Canadian magician Dai Vernon was so skilled in sleight of hand that he once fooled the legendary Harry Houdini, who could not detect how the trick was accomplished, even after watching Vernon perform it multiple times. Vernon and other magicians perfected the art of misdirection, making coins vanish or cards appear in impossible places — all while the audience’s eyes were fixed on the wrong thing. Their tricks relied on one crucial insight: if you control where people look, you can convince them that reality is something entirely different.Unfortunately, today’s fraudsters are just as clever, but their audience is far less entertained. Instead of dazzling with illusion, they use tactics like check washing, playing on distraction and trust to make money disappear from business accounts. Payment fraud has become an especially big problem in the last several years, according to Nasdaq Verafin’s 2024 Global Financial Crime Report, resulting in losses of $21B across the Americas in 2023. Meanwhile, 94% of bank executives reported being impacted by check fraud within the past 18 months.Defining Positive PayOne of the tragedies of these statistics is that technology exists to virtually eliminate the opportunity for thieves to commit check fraud against businesses. We’re talking, of course, about Positive Pay. Positive Pay is a fraud prevention system wherein a business sends its financial institution the details of recently issued checks to be compared against any checks being deposited or cashed against the business’ account. Despite its proven effectiveness, just 29% of financial institutions say they are satisfied with their business clients’ positive pay adoption rate. The overall adoption rate is only about 35%. This low adoption rate has led to hundreds of thousands of dollars in losses for community financial institutions (CFIs). image.png209.04 KB Source: Datos Insights, Q4 2023 Consider check washing, the most common type of check fraud. Here, thieves steal legitimate checks and use chemicals to “wash” them by erasing the payee's name and changing it to themselves. Positive Pay makes check washing almost impossible to pull off by comparing the check number, dollar amount, and payee name on the check presented for payment to the information that’s on the check issuance file submitted by the business to the financial institution. If there are any discrepancies, the check is flagged for further inspection.Causes of Low Positive Pay AdoptionSo, why are Positive Pay adoption rates so low? According to the latest report from Datos Insights, the main reasons are the following:

Offering business customers Positive Pay is reactive (42%). Some CFIs don’t offer Positive Pay to businesses until after check fraud has occurred.

Unintuitive for customers to initiate (35%). In some cases, it’s not seamless or easy for business customers to adopt Positive Pay within their CFI’s current interface.

Customer lack of awareness (23%). Nearly one-quarter of small- and mid-sized businesses said that their financial institution has not mentioned Positive Pay to them.

Strategies To Boost Adoption RatesHere are four strategies to increase adoption of Positive Pay at your CFI before businesses become fraud victims:

Educate your business customers about check fraud risks. Even with the growing prevalence of check fraud, many businesses don’t comprehend their exposure — just 34% say they’re very concerned about fraud. So make fraud education a high priority by hosting informational seminars and webinars, sharing anonymous check fraud case studies, embedding fraud alerts and banners on your website, and highlighting the cost of check fraud as not just financial, but also carrying reputational and operational costs.

Make Positive Pay a default option during new client onboarding. Instead of presenting Positive Pay as an optional add-on, you might find it more beneficial to make it a default that businesses must opt out of instead of into. Include Positive Pay setup during treasury onboarding and train your staff to position it as a value-added enhancement, not just a compliance requirement.

Bundle Positive Pay with other fraud protection tools. For example, a multi-pronged fraud prevention strategy might include multi-factor authentication (MFA), behavioral analytics, and ACH Positive Pay. You could bundle these together into a tiered treasury service offering and position it as a layered security product suite.

Simplify Positive Pay usage. Providing a daily check issuance file to the bank can be laborious for small businesses that aren’t using an enterprise resource planning platform. Look for ways to simplify this process — by adding integrations to more systems, for example, or an application programming interface (API) file that makes it easier to generate a check issuance file.

Be Proactive in Combatting Check FraudThe problem of check fraud isn’t going away — if anything, it will only get worse as thieves devise more technologically sophisticated ways to steal money from businesses. This makes it critical that CFIs be proactive in helping businesses reduce or eliminate check fraud by adopting technology tools like Positive Pay and making the offering more widely available and known to business customers.

The Fee Income Lever CFIs Underuse Larger banks are pulling ahead on fee income while community banks lean on the same 20% share they held in 2019. The gap is getting costly.

Turning The Small Business Succession Wave Into Deal Flow A massive SMB succession wave, amplified by the SBA doubling acquisition loan limits, creates opportunity for CFIs. This article discusses how they can make the most of the moment.

This website uses cookies to provide a personalized, informative web experience,

and to support our daily operations with your financial institution.

PCBB does not share or sell your data to other parties.

Please read our Privacy Notice to learn more about the information we collect.